2025 reminded investors of an uncomfortable truth: diversification is hardest to achieve precisely when it is needed most - during periods of stress, drawdowns, and rising correlations.

By: Robert Koloshuk

Chief Investment Officer at WaveFront GAM

The year began with optimism, but it shifted abruptly following the U.S. announcement of tariffs, which led to investor de-risking. However, the year ended with renewed optimism across equity markets. For many portfolios, the journey felt familiar - strong performance when the focus was on earnings growth, followed by sharper-than-expected drawdowns when geopolitical risks flared up.

The WaveFront All-Weather Fund is built for all environments, including major equity bear markets, but it still navigated the risk-off and risk-on whipsaw experienced in 2025 quite admirably.

What follows is a look at how the strategy navigated 2025, why certain components detracted or contributed when they did, and why the portfolio behaved differently than traditional balanced or equity-heavy allocations.

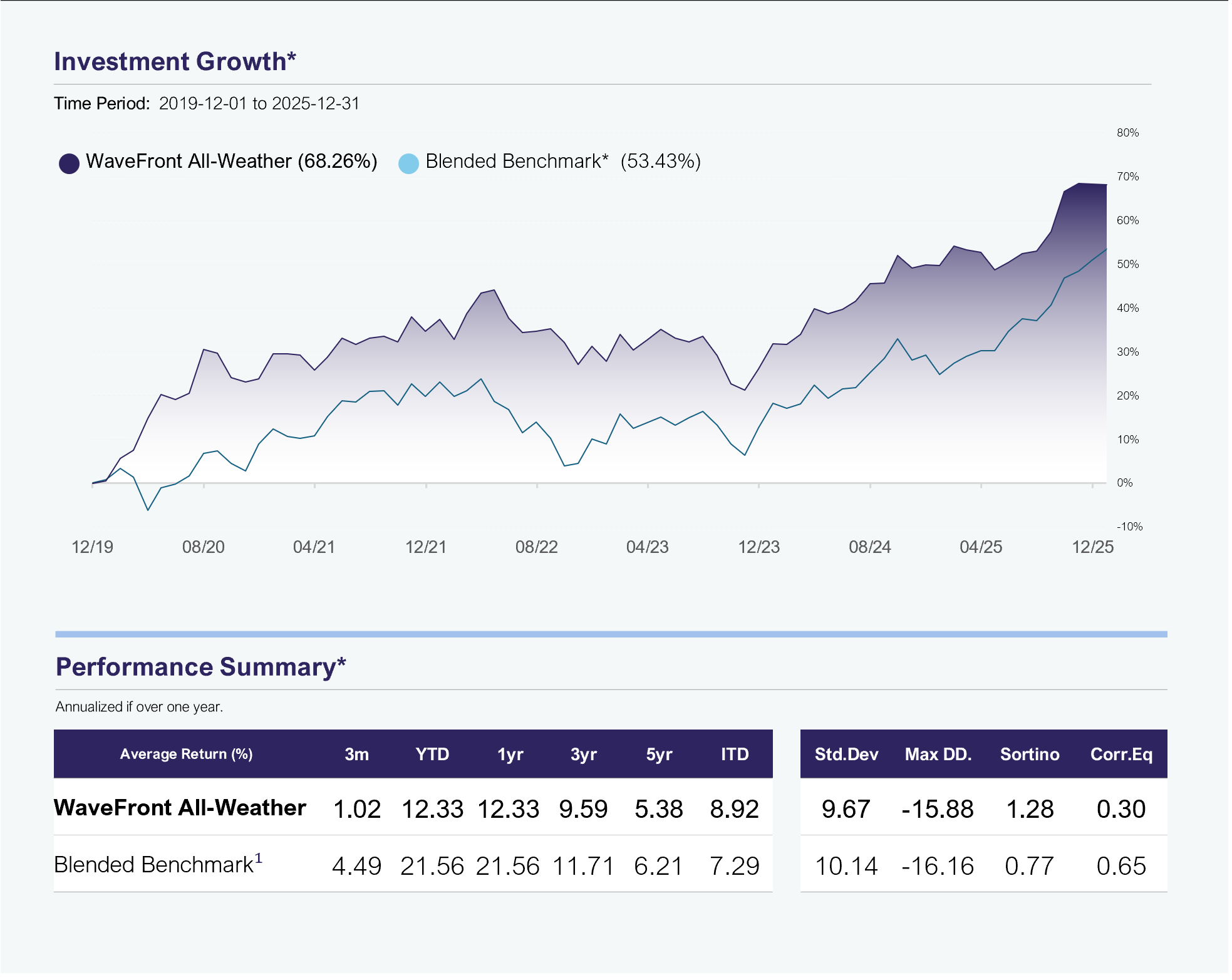

The WaveFront All-Weather Alternative Fund returned 12.3% in 2025, with 8.9% annualized net return since inception, and a +8% trailing 12-month cash yield for 2025.

Performance Highlights - as of December 31, 2025*

* Performance Disclaimer

*Performance is past performance and does not guarantee future results. Data Source: WaveFront & Bloomberg. Blended Benchmark Constituents: 20% SG CTA PR USD, 20% iShares MSCI ACWI ETF, 20% S&P GSCI Precious Metal TR, 20% Morningstar Canada REIT GR USD, 20% iShares 20+ Yr Treasury Bond ETF.

CIO Insights: Gold and correlations

One of the more unusual dynamics in 2025 was the Fund’s higher-than-expected 250-day correlation to the S&P/TSX Composite, despite having no Canadian equities other than an allocation to Canadian REITs. Over the year, the Fund showed a correlation of 0.68 to the TSX, even though the portfolio averaged roughly 18% in global equities, 20% in Canadian REITs, with the balance allocated to Managed Futures, fixed income, gold, and our special situations options strategy.

We believe this was largely driven by international capital flows tied to the rally in gold. Gold rose approximately 63% in 2025, and with the TSX comprised of nearly 40% of the world's public mining companies, strong gold performance tends to pull foreign institutional capital into Canadian markets more broadly. This can temporarily raise correlations between otherwise distinct assets.

Given gold’s significant contribution to WAAV’s performance in 2025, we’ve received questions about why we access gold exposure primarily through futures rather than ETFs or gold equities. It’s important to clarify that we are not structurally bullish on gold. In fact, gold has the lowest long-term return expectation of any sub-strategy in WaveFront All-Weather, with our forecast being roughly in line with inflation over time. Because the Fund has limits on direct leverage, we use futures selectively as the most cost-efficient way to achieve optimal exposure across asset classes. Futures represent the lowest available cost of financing, and it is sensible to minimize financing costs in the sub-strategy with the lowest expected return. Leveraging a gold ETF would knowingly impose higher borrowing costs on a position where we expect modest long-term returns. While gold experienced a powerful rally in 2025, this was not a tactical call, it was part of the Fund’s long-term design and delivering income rather than paying higher borrowing costs to generate capital gains is consistent with our design of the fund. This means we can deliver superior headline performance versus funds that borrow at higher costs to obtain their target risk exposure.

Despite the elevated TSX correlation observed in 2025, All-Weather remains fundamentally superior to balanced funds for downside protection and performance in risk-off environments.

The strategy aims to deliver a combination of income and capital appreciation without sacrificing long-term total returns. While distributions may vary from quarter to quarter, we believe this approach ultimately delivers more income over full market cycles than funds engineered to maintain artificially stable dividend payouts.

A core principle of the strategy is avoiding return-of-capital distributions, which is why we use variable quarterly payments. This flexibility allows us to maximize income over time while minimizing ROC risk – an important consideration for advisors working with registered accounts, family offices, foundations, and investors in decumulation mode.

We believe many investors unknowingly give up long-term returns in pursuit of capital gains treatment that may not even be optimal for their tax situation. All-Weather offers a more efficient way to generate income at the highest possible rate, without taking undue risk. For clients with a medium-risk tolerance and concerns about the global economy, All-Weather remains a highly defensive means of generating income while protecting against major bear markets like the 2008 Global Financial Crisis.

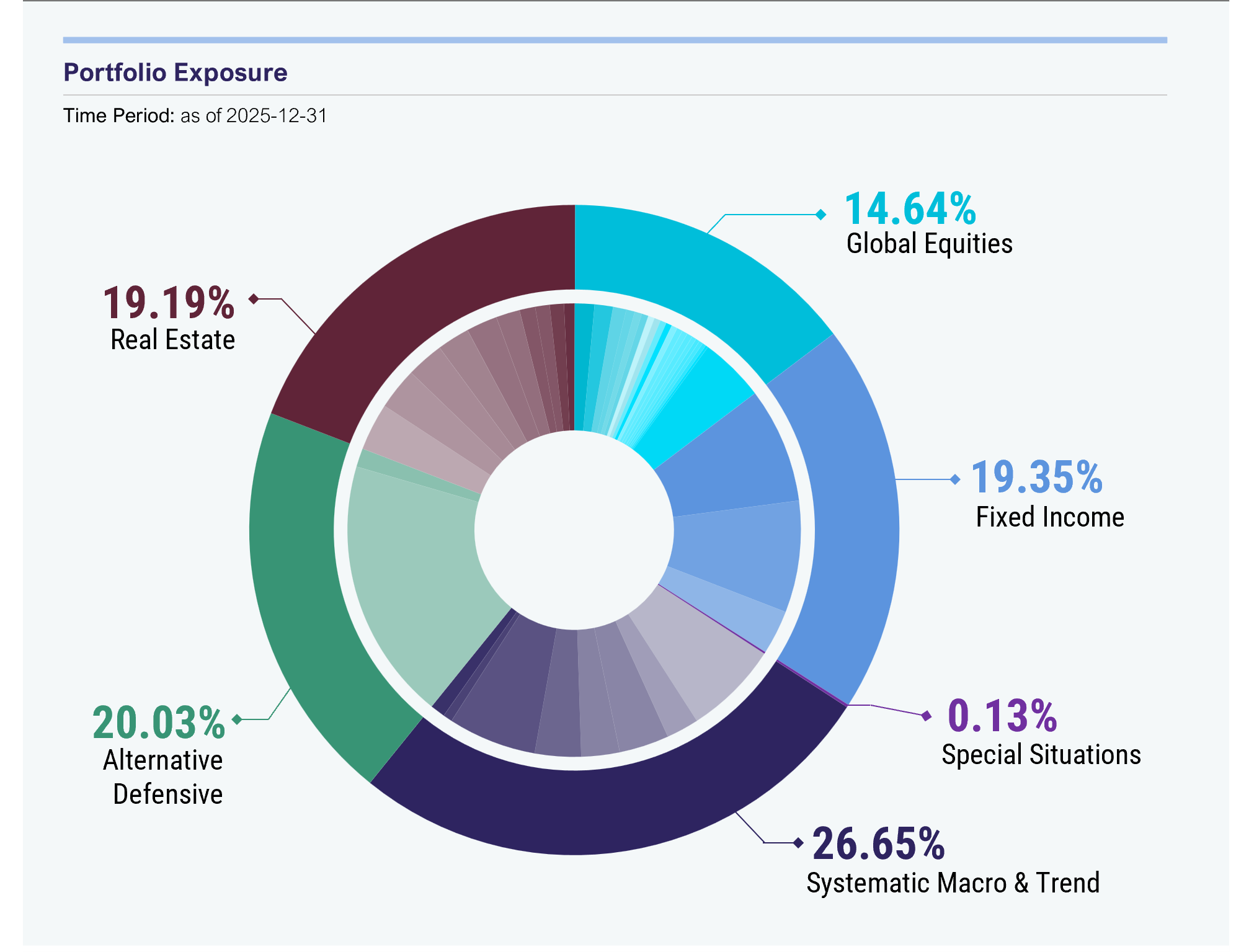

Portfolio Highlights - as of December 31, 2025*

* Portfolio Disclaimer

*Performance is past performance and does not guarantee future results. Data Source: WaveFront & Bloomberg. Portfolio exposure and holdings are as of Dec 31, 2025. Portfolio holdings and sectors will fluctuate over the life of the mutual fund as the portfolio holdings and market value of each security changes. The portfolio manager(s) may change the portfolio allocations in some or all of the sectors.

How WaveFront All-Weather is Positioned

The portfolio remains diversified across five core sleeves - Global Equities, Fixed Income, Real Estate, Systematic Macro & Trend, and Alternative Defensive - with risk budgets calibrated through our proprietary volatility-forecasting and correlation framework.

What matters most is not any single sleeve weight, but the portfolio’s overall balance between participation and protection, and its ability to adapt as correlations change. When markets are calm and trends are durable, the portfolio can lean into return-seeking exposures. When volatility rises or correlations compress diversification benefits, the portfolio systematically shifts its risk posture.

A final point worth emphasizing: WAAV was designed with an institutional lens perspective. Many institutional portfolios operate in non-taxable or tax-sheltered structures, where the priority is the quality of the return stream - stability, resilience, and the ability to rebalance through volatility - rather than optimizing for capital gains treatment. For many Canadian investors, this same lens is increasingly relevant because a significant portion of household wealth is held in registered accounts, where portfolio decisions can focus on long-term outcomes rather than near-term tax frictions.

Risk management: why “looks diversified” isn’t always diversified

A recurring theme in our conversations with advisors is that many portfolios appear conservative based on labels (e.g., “alts,” “income,” “low-vol”), but the underlying exposures often behave like equity risk in disguise…. particularly in stressed markets when correlations rise.

WAAV approaches risk differently. The strategy is built to avoid relying on any single “story” (rates down, growth up, gold hedge, etc.). Instead, it uses systematic risk budgeting and diversification across structurally different return sources, paired with convex hedging tools designed for fast-moving shock windows where traditional systematic strategies may not adjust quickly enough.

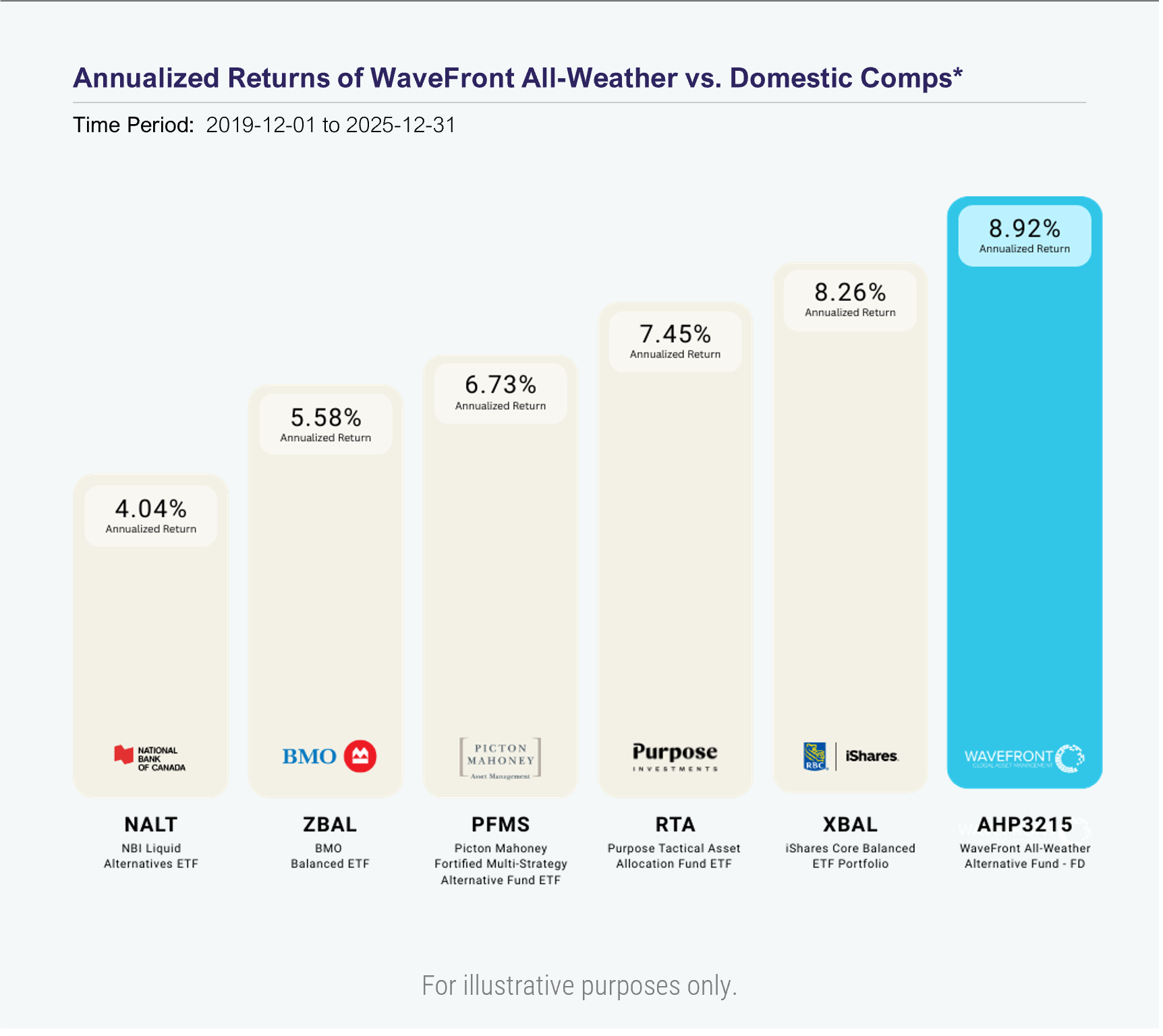

The WaveFront All-Weather Alternative Fund has consistently outperformed its peer group, delivering superior returns and value to our investors*

* Performance Disclaimer

*Performance is past performance and does not guarantee future results. Data Source: WaveFront & Bloomberg. Blended Benchmark Constituents: 20% SG CTA PR USD, 20% iShares MSCI ACWI ETF, 20% S&P GSCI Precious Metal TR, 20% Morningstar Canada REIT GR USD, 20% iShares 20+ Yr Treasury Bond ETF.

Looking ahead: the case for staying adaptable

If 2025 taught anything, it’s that markets can stay “risk-on” longer than expected — and then reprice quickly when the narrative shifts. Policy expectations, inflation surprises, and correlation behavior remain key variables, and the most important risk is not a bad month, it’s being structurally unprepared for a regime change.

WAAV’s job is not to predict the next inflection point. It’s to remain positioned to participate when conditions are constructive and to defend early when correlations and volatility rise, using systematic rebalancing for evolving trends and convex hedges for sudden events.

What investors should remember: WAAV is engineered to balance participation and protection, so investors can stay invested through uncertainty without betting the farm on a single macro outcome. Whether 2026 is another year of AI dominance, a continuation of the rally in precious metals, or a dramatic end to both of those narratives, WAAV is able to navigate that uncertainty.

About the WaveFront All-Weather Alternative Fund

Introducing Canada's premiere all-weather investment solution, the WaveFront All-Weather Alternative Fund. Engineered to deliver stability and consistent performance, regardless of the market environment, now available as both a mutual fund and ETF.

The WaveFront All-Weather Alternative Fund is engineered to deliver consistent, superior risk-adjusted returns across diverse market conditions. With a dynamic multi-asset and multi-strategy approach, it offers a next-generation liquid alternative designed for stability and growth.

IMPORTANT DISCLAIMER: For the period from inception to December 31, 2024, the performance data of Series ETF reflects the historical return of the LP, which for this period had substantially similar fees as the LP. Effective January 2, 2025, WaveFront All-Weather Fund, LP (“the “LP”) was merged into WaveFront All-Weather Alternative Fund. Prior to the merger, the LP was distributed to investors on a prospectus-exempt basis in accordance with National Instrument 45-106 and was not a reporting issuer from its inception on November 1, 2019 until the merger. Financial statements of the LP are posted on Arrow’s website and are available to investors upon request.

Commissions, trailing commissions, management and performance fees and expenses all may be associated with mutual fund investments. Please read the prospectus before investing. The indicated rates of return are the historical annual compound total returns net of fees and expenses payable by the fund (except for figures of one year or less, which are simple total returns) including changes in security value and reinvestment of all distributions and do not take into account sales, redemption, distribution or optional charges or income taxes payable by any securityholder that would have reduced returns. Mutual funds are not guaranteed, their values change frequently and past performance may not be repeated.

The risk level of a fund has been determined in accordance with a standardized risk classification methodology in National Instrument 81-102, that is based on the fund’s historical volatility as measured by the 10-year standard deviation of the fund’s returns. Where a fund has offered securities to the public for less than 10 years, the standardized methodology requires that the standard deviation of a reference mutual fund or index that reasonably approximates the fund’s standard deviation be used to determine the fund’s risk rating. Please note that historical performance may not be indicative of future returns and a fund’s historical volatility may not be indicative of future volatility. The rates of return are used only to illustrate the effects of the compound growth rate and are not intended to reflect future values or returns on an investment fund. The Investment Growth chart shows the final value of a hypothetical investment in securities in this series of the fund as at the end of the investment period indicated and is not intended to reflect future values or returns on investment in such securities. The comparison presented is intended to illustrate the historical performance of the fund as compared with the historical performance of a widely quoted market index or a weighted blend of widely quoted market indices. There are various important differences that may exist between the fund and the stated indices that may affect the performance of each. The objectives and strategies of the fund result in holdings that do not necessarily reflect the constituents of and their weights within the comparable indices. Indexes are unmanaged and their returns do not include any sales charges or fees. It is not possible to invest directly in market indices.