Participate in the Upside. Prepared for the Downside.

By: Robert Koloshuk

Chief Investment Officer at WaveFront GAM

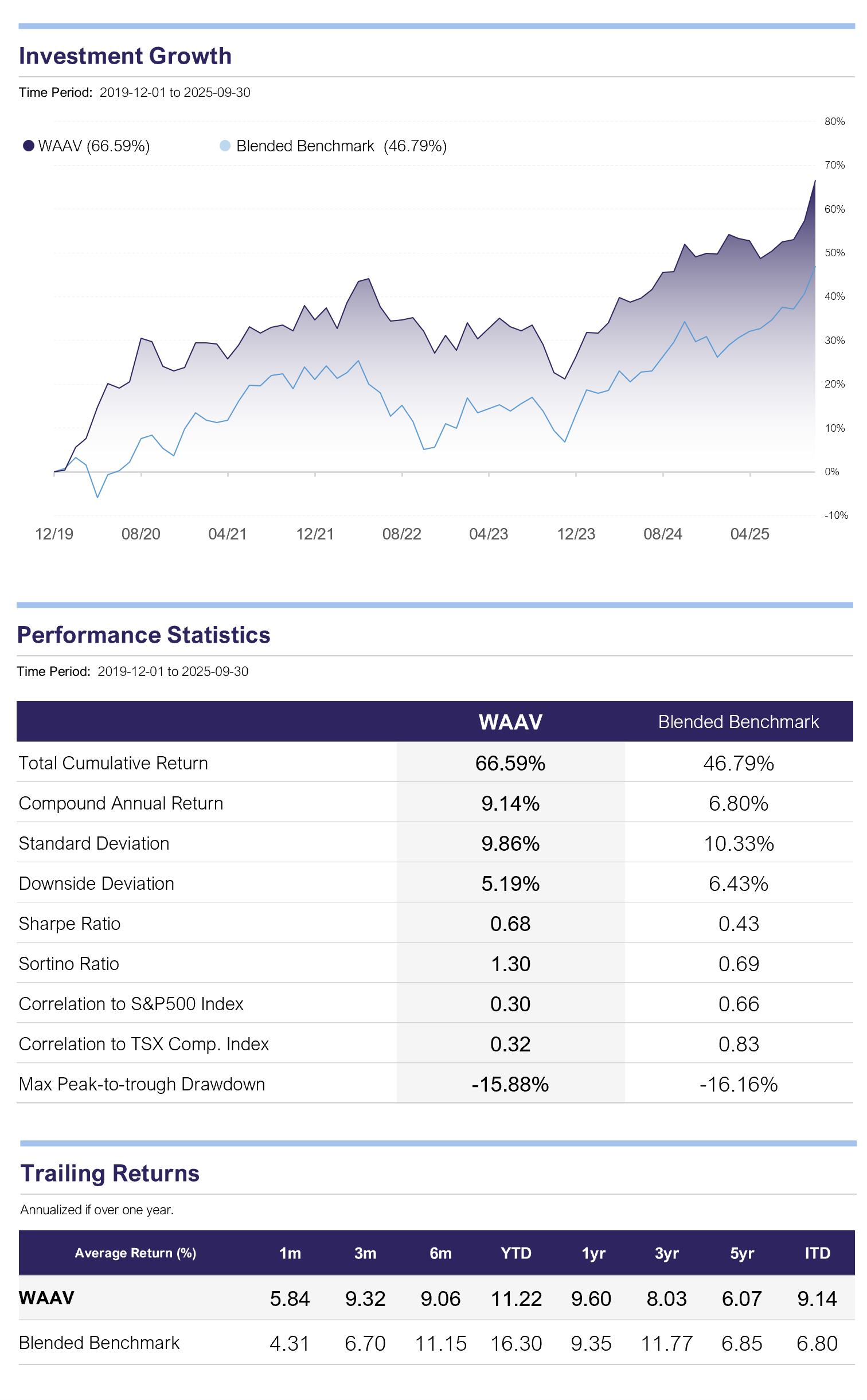

The WaveFront All-Weather Alternative Fund ETF (WAAV) gained +5.82% in September and +9.28% for Q3, bringing year-to-date performance to +11.18% (as of 9/30). The fund continues to deliver equity-like returns with a lower correlation and volatility than balanced funds.

Performance was broad-based across all asset class sleeves. Alternative Defensive was the top contributor in the quarter, doing its job in choppy markets while contributing some additional convexity via its allocation to Gold. Systematic Macro & Trend also produced strong results as commodity volatility resurfaced, particularly in metals. Global Equities and Real Estate benefited from the risk-on impulse tied to falling policy-rate expectations, while Fixed Income contributed positively as interest rates declined. Special Situations remained flat, with no active exposure during the period.

Performance Highlights - as of September 30, 2025*

* Performance Disclaimer

*Performance is past performance and does not guarantee future results. Data Source: WaveFront & Bloomberg. Blended Benchmark Constituents: 20% SG CTA PR USD, 20% iShares MSCI ACWI ETF, 20% S&P GSCI Precious Metal TR, 20% Morningstar Canada REIT GR USD, 20% iShares 20+ Yr Treasury Bond ETF.

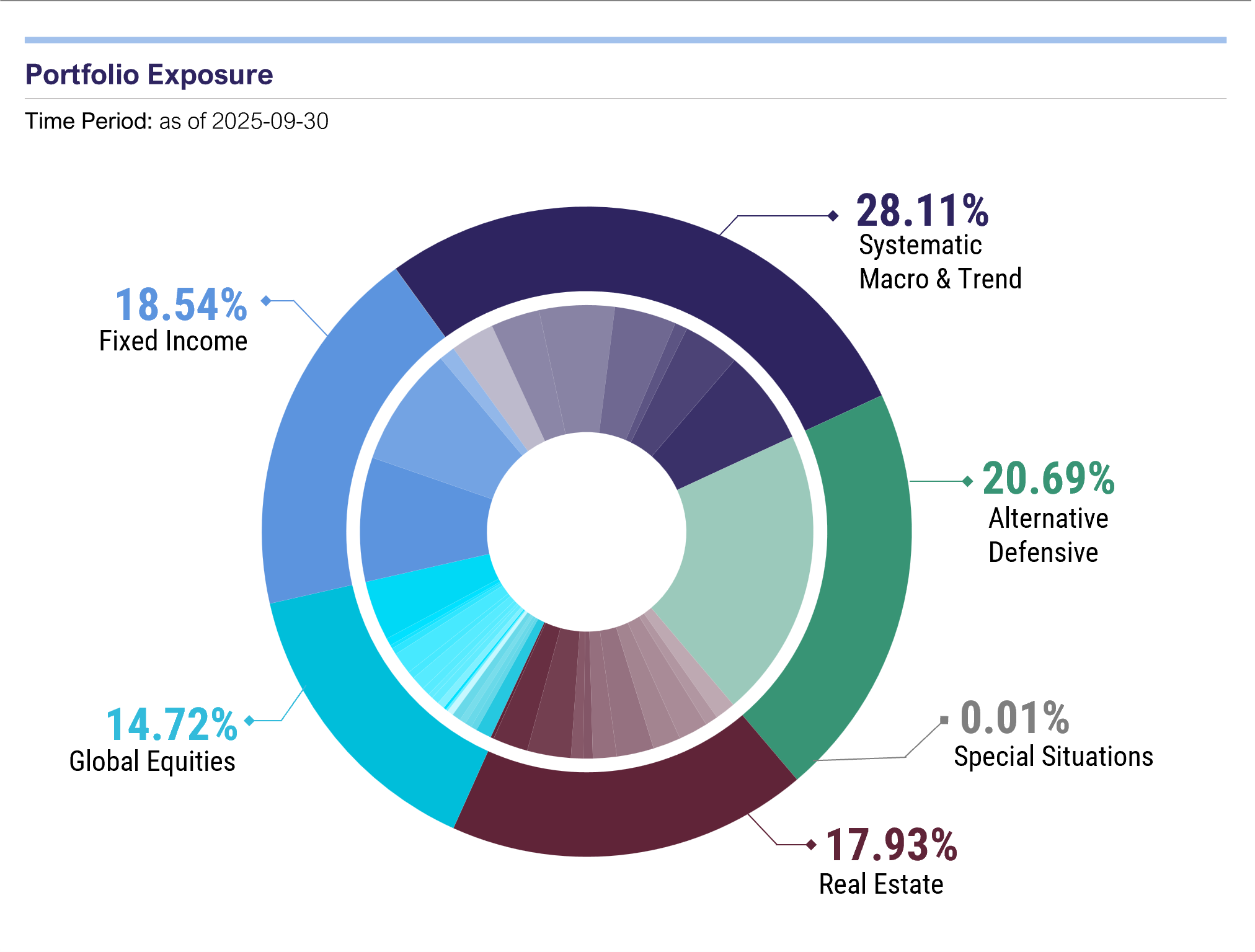

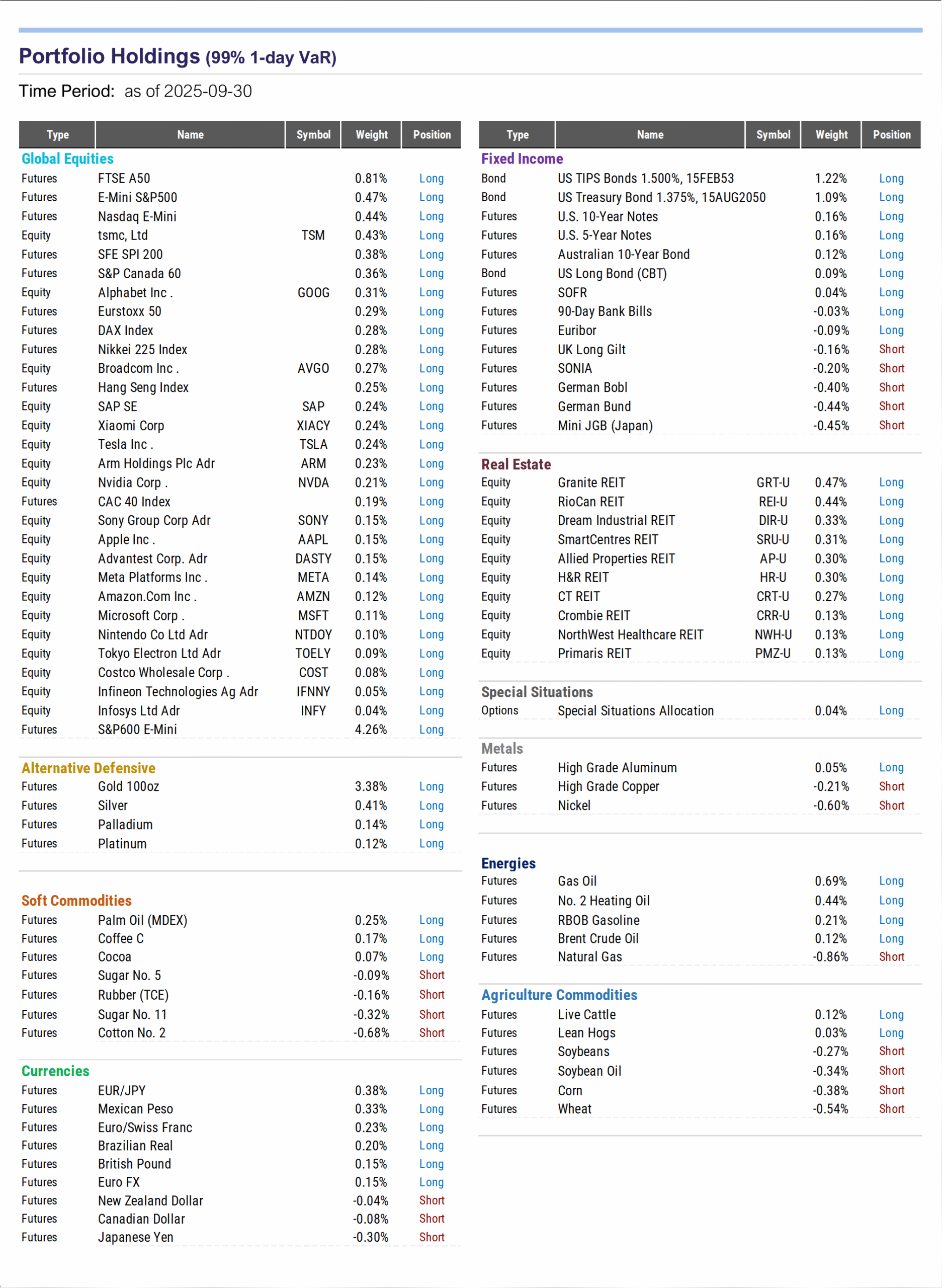

How WAAV is Positioned

The portfolio remains broadly diversified across five core asset class sleeves - Global Equities, Fixed Income, Real Estate, Systematic Macro & Trend, and Alternative Defensive - with risk budgets calibrated through our proprietary volatility-forecasting and correlation framework.

During the quarter, modest rebalancing shifts were implemented to maintain equilibrium in risk-on vs. risk-off exposures as intermarket correlations were rising.

Equity exposure remains concentrated in large cap and technology-oriented stocks that continue to demonstrate relative strength amid expectations for lower policy rates. It has historically been easier for the WAAV model to identify volatility shocks in these types of equities, which increases the likelihood of being able to deallocate beneficially in a crisis. Fixed income exposure has been increased, and within real estate, we maintain a defensive bias toward high-cash-flow names with larger, diversified portfolios of properties.

The Systematic Macro & Trend sleeve continues to express medium-term strength in precious metals, while maintaining tactical flexibility to reduce exposure if momentum falters or if volatility rises. Alternative Defensive strategies - our primarily tail-risk hedging component, has been generating substantial performance from Gold, but we have gradually redeployed some risk budget toward opportunistic hedges using deep out-of-the-money options. These positions are designed to provide asymmetric upside during periods of rapid regime transition, such as a sudden policy reversal or inflation surprise.

Portfolio Highlights - as of September 30, 2025*

* Portfolio Disclaimer

*Performance is past performance and does not guarantee future results. Data Source: WaveFront & Bloomberg. Portfolio exposure and holdings are as of May 31, 2025. Portfolio holdings and sectors will fluctuate over the life of the mutual fund as the portfolio holdings and market value of each security changes. The portfolio manager(s) may change the portfolio allocations in some or all of the sectors.

Overall, the strategy is positioned for a “late-cycle” environment characterized by declining nominal growth, easing policy expectations, and cross-asset volatility suppression that could unwind quickly. Our goal remains unchanged: to deliver stable, risk-adjusted returns across diverse market conditions by dynamically adjusting exposures rather than making binary macro calls on the stock market.

CIO Insights: Market Context & Outlook

Markets remain highly sensitive to the path of interest rates. The disappearance of 5% GICs has redirected capital toward risk assets, driving renewed strength in equities and precious metals. The key risk on the horizon is a surprise uptick in inflation, particularly in a period when official data releases remain limited or delayed. Such a scenario could trigger simultaneous drawdowns across both stocks and metals.

While the recent surge in silver prices has been notable, it is not unprecedented, and further upside remains possible; however, short-term pullbacks of 15-20% are equally plausible. The strategy’s systematic sleeve is designed to adapt to shifting market regimes, while the planned deployment of deep out-of-the-money hedges adds protection against sudden reversals during the first 48 to 72 hours of a shock event, a brief period in which Systematic Macro & Trend may not be effective at managing downside.

Looking Ahead: All-Weather Means Always Ready

As we move into the final quarter of the year, markets are finely balanced between optimism over easier policy and the risk of a policy surprise. The CME FedWatch tool and SOFR prices indicate a 95% probability of more rate cuts in 2025, but expectations baked into markets may be too one-sided. Any signal of rising inflation, or the possibility that the Federal Reserve delays or even reverses course, will quickly unsettle the “risk-on” environment that has fueled strong gains across equities, real estate, and precious metals.

For the All-Weather strategy, the focus remains on maintaining balance between participation and protection. We expect continued dispersion across asset classes as growth and inflation diverge globally, creating opportunities for systematic macro positioning. At the same time, we are reinforcing our defensive toolkit through the selective use of deep out-of-the-money options to offset concentrated exposures if volatility returns suddenly. The combination of diversified sources of return, adaptive risk budgeting, and disciplined hedging leaves the strategy well positioned to navigate the next phase of the cycle, regardless of whether the fourth quarter extends the current rally or tests the durability of investor confidence.

About the WaveFront All-Weather Alternative Fund

Introducing Canada's premiere all-weather investment solution, the WaveFront All-Weather Alternative Fund. Engineered to deliver stability and consistent performance, regardless of the market environment, now available as both a mutual fund and ETF.

The WaveFront All-Weather Alternative Fund is engineered to deliver consistent, superior risk-adjusted returns across diverse market conditions. With a dynamic multi-asset and multi-strategy approach, it offers a next-generation liquid alternative designed for stability and growth.

IMPORTANT DISCLAIMER: For the period from inception to December 31, 2024, the performance data of Series ETF reflects the historical return of the LP, which for this period had substantially similar fees as the LP. Effective January 2, 2025, WaveFront All-Weather Fund, LP (“the “LP”) was merged into WaveFront All-Weather Alternative Fund. Prior to the merger, the LP was distributed to investors on a prospectus-exempt basis in accordance with National Instrument 45-106 and was not a reporting issuer from its inception on November 1, 2019 until the merger. Financial statements of the LP are posted on Arrow’s website and are available to investors upon request.

Commissions, trailing commissions, management and performance fees and expenses all may be associated with mutual fund investments. Please read the prospectus before investing. The indicated rates of return are the historical annual compound total returns net of fees and expenses payable by the fund (except for figures of one year or less, which are simple total returns) including changes in security value and reinvestment of all distributions and do not take into account sales, redemption, distribution or optional charges or income taxes payable by any securityholder that would have reduced returns. Mutual funds are not guaranteed, their values change frequently and past performance may not be repeated.

The risk level of a fund has been determined in accordance with a standardized risk classification methodology in National Instrument 81-102, that is based on the fund’s historical volatility as measured by the 10-year standard deviation of the fund’s returns. Where a fund has offered securities to the public for less than 10 years, the standardized methodology requires that the standard deviation of a reference mutual fund or index that reasonably approximates the fund’s standard deviation be used to determine the fund’s risk rating. Please note that historical performance may not be indicative of future returns and a fund’s historical volatility may not be indicative of future volatility. The rates of return are used only to illustrate the effects of the compound growth rate and are not intended to reflect future values or returns on an investment fund. The Investment Growth chart shows the final value of a hypothetical investment in securities in this series of the fund as at the end of the investment period indicated and is not intended to reflect future values or returns on investment in such securities. The comparison presented is intended to illustrate the historical performance of the fund as compared with the historical performance of a widely quoted market index or a weighted blend of widely quoted market indices. There are various important differences that may exist between the fund and the stated indices that may affect the performance of each. The objectives and strategies of the fund result in holdings that do not necessarily reflect the constituents of and their weights within the comparable indices. Indexes are unmanaged and their returns do not include any sales charges or fees. It is not possible to invest directly in market indices.